Klarna Chargebacks Explained: Protect Your Revenue

Klarna pays you upfront. But that does not mean you are insulated from disputes. Klarna chargebacks follow their own rules, their own timelines, and their own evidence standards — and missing any one of them is an automatic loss. This guide explains exactly how the process works, why disputes happen, and what you can do to reduce them before they cost you.

How Klarna Chargebacks Differ From Card Disputes

Traditional card chargebacks run through Visa or Mastercard networks. Klarna disputes do not. Because Klarna acts as the buyer's lender and pays you directly, disputes go through their own internal process. Understanding that distinction changes everything about how you prepare.

Klarna is the intermediary

When a buyer disputes a Klarna purchase, they contact Klarna — not their bank and not you directly. Klarna investigates the claim and then contacts you. The card networks are not involved. Klarna sets the rules, the timelines, and the evidence standards.

Klarna absorbs some fraud risk — but not all

For orders Klarna has approved and paid out, Klarna absorbs liability for certain types of fraud (e.g. identity theft where Klarna made the credit decision). However, if the dispute relates to delivery, product quality, or merchant error, you are still liable.

Short timelines and strict evidence requirements

Klarna typically gives merchants around seven days to respond to a dispute with supporting evidence. Miss the window and you lose automatically — regardless of how strong your case actually is. There is no appeals buffer for late responses.

Different reason codes than card chargebacks

Klarna uses its own internal dispute categories: item not received, item not as described, return not processed, and duplicate charge are the most common. Each category requires different evidence and a different approach to winning.

The Full Klarna Dispute Lifecycle

Knowing each stage of the dispute process tells you exactly where to focus your prevention and preparation efforts.

Buyer Opens a Dispute

The buyer contacts Klarna through the Klarna app or website to raise a complaint. Common triggers: they say the item never arrived, the item looks different from what was shown, they returned it but payment continued, or they claim they never made the purchase.

Klarna Pauses Buyer Payments

Klarna immediately pauses the buyer's instalment payments while the dispute is under review. This protects the buyer during the investigation period. For you as the merchant, this can signal an imminent chargeback if the dispute is not resolved quickly.

Klarna Notifies You

You receive a dispute notification via your merchant portal (or via Shopify if using the Klarna payment integration). From this point, your response clock starts. Treat this as a critical ticket — not a support request.

You Submit Evidence

You have approximately seven days to submit your evidence package. This includes proof of delivery, order confirmation, tracking history, customer communications, and your published return policy. Incomplete submissions are treated the same as no submission.

Klarna Reviews and Decides

Klarna evaluates your evidence against the buyer's claim using their internal review criteria. They may ask follow-up questions. The decision is typically issued within 14 to 30 days of the dispute being raised.

Funds Are Settled or Clawed Back

If Klarna finds in the buyer's favour, the chargeback amount is deducted from your next settlement. If they find in your favour, the dispute is closed and your payout is protected. There is no card network arbitration stage — Klarna's decision is final in most cases.

Why Klarna Chargebacks Happen: The 4 Root Causes

Most Klarna disputes trace back to one of four operational gaps. Fixing them at the source is the highest-leverage thing you can do to protect revenue.

Item Not Received

Most commonThe buyer claims the order never arrived. This is the most frequent dispute type and the most winnable — if you have tracking. Orders shipped without carrier scan history, with last-mile delivery gaps, or with no signature on high-value items are the most vulnerable. Carriers marking items as delivered when they were not is also a major trigger.

- Use tracked shipping on every Klarna order, no exceptions

- Add signature-required for orders above your average order value threshold

- Send proactive delivery updates at shipped, out-for-delivery, and delivered stages

- Use carriers with reliable scan history for your key routes

Item Not As Described

High volumeThe buyer received something — but it does not match what was shown or described on your product page. BNPL buyers often make faster purchase decisions, relying heavily on hero images and brief descriptions. Variant mismatches (wrong size, wrong colour), inaccurate dimensions, missing components, and vague product copy all drive this dispute category.

- Use real, unretouched photos that show scale, texture, and colour accurately

- Add size guides, fit notes, and dimension tables to all relevant product pages

- Make variant selection explicit in order confirmation emails (not just "Product A")

- Add "what is included in the box" sections for multi-component products

Return Not Processed

BNPL-specificThe buyer returned the item but Klarna continued charging their instalments. This is a BNPL-specific dispute type that rarely exists in card transactions. The gap usually happens because the merchant processed a refund in their own system but did not trigger the corresponding refund in the Klarna merchant portal, leaving Klarna unaware and the buyer still being charged.

- Process all Klarna refunds through the Klarna merchant portal — not just your Shopify admin

- Add BNPL refund timelines and instalment pause language to order confirmation emails

- Set a 48-hour SLA for processing returns from date of receipt

- Train support staff on the distinction between a standard refund and a Klarna refund

Fraud and Unauthorised Transactions

Growing riskA buyer (or someone using stolen identity) claims they never made the purchase. Where Klarna approved the credit decision based on their own risk assessment, they absorb the fraud liability. However, if fraud signals were present at order time that you ignored — suspicious shipping addresses, mismatched billing, unusually high basket values from new accounts — Klarna may hold you partially liable depending on their investigation outcome.

- Activate Shopify Fraud Analysis and review scores on all Klarna orders

- Build rules to hold orders with high fraud scores for manual review

- Focus scrutiny on first-time buyers, rush shipping, and high-value baskets

- Never fulfil a flagged order just to hit shipping targets

How to Reduce Klarna Chargebacks: The Prevention Playbook

Prevention is always cheaper than winning disputes. Here is the operational framework that consistently reduces chargeback volume.

Delivery Proof is Your Primary Defence

- Ship every Klarna order with a tracked service — untracked shipping is indefensible in disputes

- Require signatures for orders above your dispute risk threshold (start with your top 20% by order value)

- Automate email or SMS notifications at three stages: shipped, out for delivery, delivered

- Screenshot and store carrier tracking pages at the point of delivery — not days later when evidence is needed

- Choose carriers with reliable scan history on routes where you have had previous delivery disputes

Make Return and Refund Policy Unmissable

- Display your full return policy at checkout, not buried in a footer link

- Include BNPL-specific refund language in order confirmation emails: "If you return this item, your Klarna payment schedule will be paused within X days of us processing your return"

- State exact refund timelines — "within 5 business days of receiving your return" — not vague language

- For Klarna refunds, initiate the refund in the Klarna merchant portal within 24 hours of confirming receipt

Close Product Description Gaps

- Audit your highest-volume Klarna SKUs for description accuracy — are dimensions, materials, and colours correctly shown?

- Add user-generated content (UGC) photos alongside studio shots to set realistic expectations

- Check that variant options (size, colour, configuration) are unambiguous in checkout and in confirmation emails

- For high-ticket items, add a "What is in the box" section and a short product video

Use Shopify Fraud Tools Proactively

- Enable Shopify Fraud Analysis on your store and review scores for every Klarna order before fulfilling

- Create automated rules to hold orders with high risk scores — do not rely on manual checks

- Flag orders with mismatched billing and shipping addresses, forwarding addresses, or multiple failed payment attempts

- Review your Fraud Control dashboard weekly and track which product categories and regions generate the most flagged orders

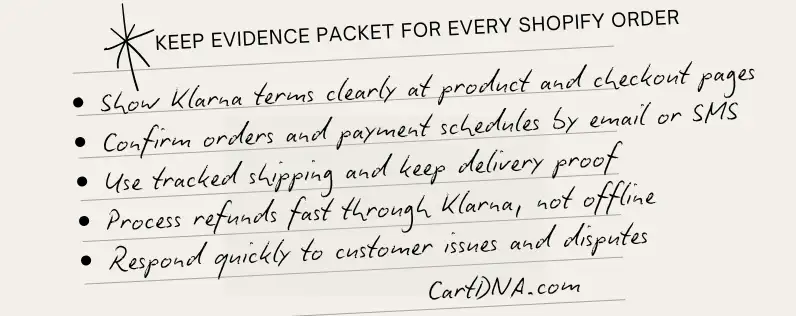

Build a Klarna Evidence Packet for Every Order

Speed is the most important factor when responding to Klarna disputes. The merchants who win consistently prepare evidence before a dispute arrives — not after they receive the notification. Build a per-order evidence file as a standard part of your fulfilment workflow.

| Evidence Item | What to Include |

|---|---|

| Order confirmation | Invoice showing SKU, variant, quantity, price, and customer name |

| Tracking information | Full carrier tracking URL plus screenshots of scan history milestones |

| Delivery confirmation | Carrier delivery confirmation and signature proof for high-value orders |

| Customer communications | Complete email or chat thread including any refund or return exchanges |

| Policy proof | Screenshot of your return and refund policy as it appeared at checkout on the purchase date |

| Return receipt (if applicable) | Date and method of return receipt, and corresponding refund initiation record in Klarna portal |

Respond before day five, not on day seven. Klarna reviewers weigh how quickly merchants respond. Late submissions — even within the window — signal poor organisation and can affect close calls.

How CartDNA Supports Your Klarna Dispute Workflow

CartDNA Shopify apps are built around the reality of BNPL dispute management. Here is how they reduce your exposure and improve your outcomes.

BNPL-Focused Risk Scoring

Orders are scored using signals specific to Klarna dispute patterns: first-time buyers, high basket values, address mismatches, and rush shipping. You reduce risky fulfilment decisions before they become disputes.

Automated Fulfilment Controls

Risk scores trigger automated actions — hold, require signature, or cancel based on rules you configure. Automation speeds decisions and removes the manual errors that let high-risk orders slip through.

Dispute Telemetry and Insights

CartDNA surfaces which SKUs, regions, and carriers drive Klarna chargeback losses. You can act on real signals: update product pages, adjust shipping choices, or change refund workflows before losses grow.

One-Click Evidence Bundles

Evidence compiles automatically per order in the format Klarna expects. You submit complete, well-organised documentation quickly. Speed plus accuracy improves win rates and reduces the manual workload on your ops team.

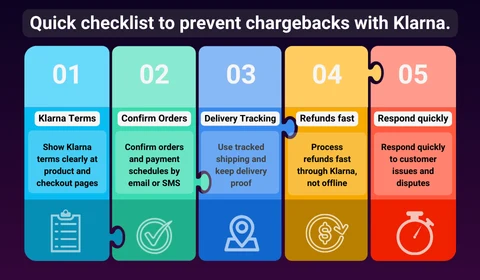

Quick Checklist: Klarna Chargeback Prevention

- Tracked shipping activated on every Klarna order

- Signature required for orders above your value threshold

- Delivery updates sent at shipped, out-for-delivery, and delivered stages

- BNPL refund timeline language in order confirmation emails

- Return and refund policy visible at checkout (not just in footer)

- All Klarna refunds processed via Klarna merchant portal within 24 hours

- Shopify Fraud Analysis enabled and reviewed before every high-risk fulfilment

- Evidence packet stored per order before the order ships

- Dispute alerts set to trigger critical-priority tickets in your team

Frequently Asked Questions

Are Klarna chargebacks the same as credit card chargebacks?

No. Klarna chargebacks bypass card networks entirely. Because Klarna acts as the lender and pays you directly, disputes go through Klarna's own internal process. The reason codes, timelines, evidence requirements, and decision-making all follow Klarna rules — not Visa or Mastercard rules. This means your existing card dispute playbook does not fully apply to Klarna cases.

How long do I have to respond to a Klarna dispute?

Typically around seven days from the date the dispute notification is issued. Missing this window results in an automatic loss regardless of the merit of your case. Klarna dispute alerts should be treated as critical priority tickets, not standard support requests. Aim to submit evidence by day five, not day seven.

Does Klarna protect merchants from fraud chargebacks?

Partially. For transactions where Klarna approved the credit decision and fraud occurred due to stolen identity, Klarna typically absorbs that liability. However, if there were fraud signals at order time that you did not act on — mismatched addresses, high-risk scores, unusual order patterns — Klarna may hold you responsible depending on their investigation. Using Shopify Fraud Analysis and holding high-risk orders before fulfilment is your best protection.

What evidence does Klarna require to win a dispute?

For item not received disputes, the primary evidence is carrier tracking showing delivery (ideally with a signature). For item not as described, you need to show that your product page accurately represented what was sent. For return-related disputes, you need refund initiation records in the Klarna portal and your return policy as it appeared at checkout. Incomplete evidence submissions are treated the same as no evidence.

Build a Klarna Dispute Process That Actually Works

The merchants who lose Klarna chargebacks consistently share the same gaps: no tracking, no evidence preparation, late responses. The merchants who win share the same habits: proof built before shipping, policies made unmissable, responses submitted early. CartDNA helps you automate the prevention layer and build the evidence workflow that makes the difference.